GST Tax Invoice (Grade A)

Summary:

This GST Tax Invoice note discusses Tax Invoice, Credit, and Debit Notes in the context of GST. It covers the types of invoices, who is liable to issue a tax invoice, the time limit for issuing a tax invoice, revised invoices, and the contents of a tax invoice. It also explains when credit and debit notes should be issued and their details, along with the manner of issuing invoices and the use of e-invoicing. The article also mentions receipt/payment vouchers and the use of the Bill of Supply instead of a Tax Invoice for exempted goods or services under the composition scheme.

Excerpt:

GST Tax Invoice (Grade A)

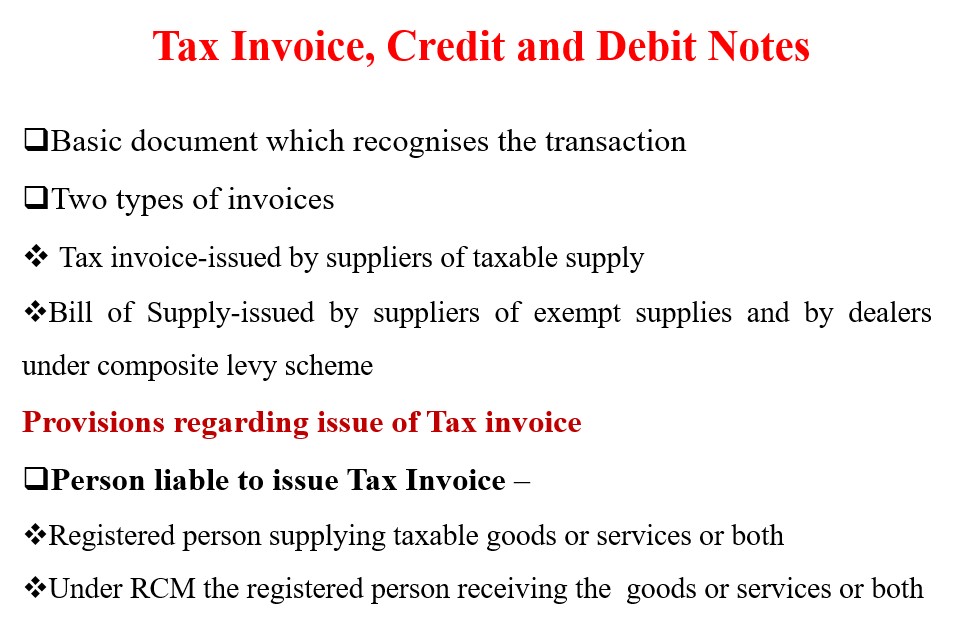

Tax Invoice, Credit and Debit Notes

- The basic document which recognizes the transaction

- Two types of invoices

– Tax invoice issued by suppliers of taxable supply

– Bill of Supply-issued by suppliers of exempt supplies and by dealers under the composite levy scheme

Provisions regarding the issue of Tax invoice

- Person liable to issue Tax Invoice

- Registered person supplying taxable goods or services or both

- Under RCM the registered person receiving the goods or services or both

The time limit for issuing of Tax Invoice

a) In case of a supply of goods

- Where the supply involves the movement of goods, before or at the time of removal of goods for supply to the recipient.

- In any other case, before or at the time of delivery of goods or making available thereof to the recipient.

b) In case of a supply of services

- In normal cases, before or after the provision of service but within a period of 30 days from the date of supply of service.

- In the case of insurance, banks, NBFCs, and Financial Institutions, before or after the provision of service but within a period of 45 days from the date of supply of service.

Reviews